Updated June 2026

What Is Liability Insurance Insurance?

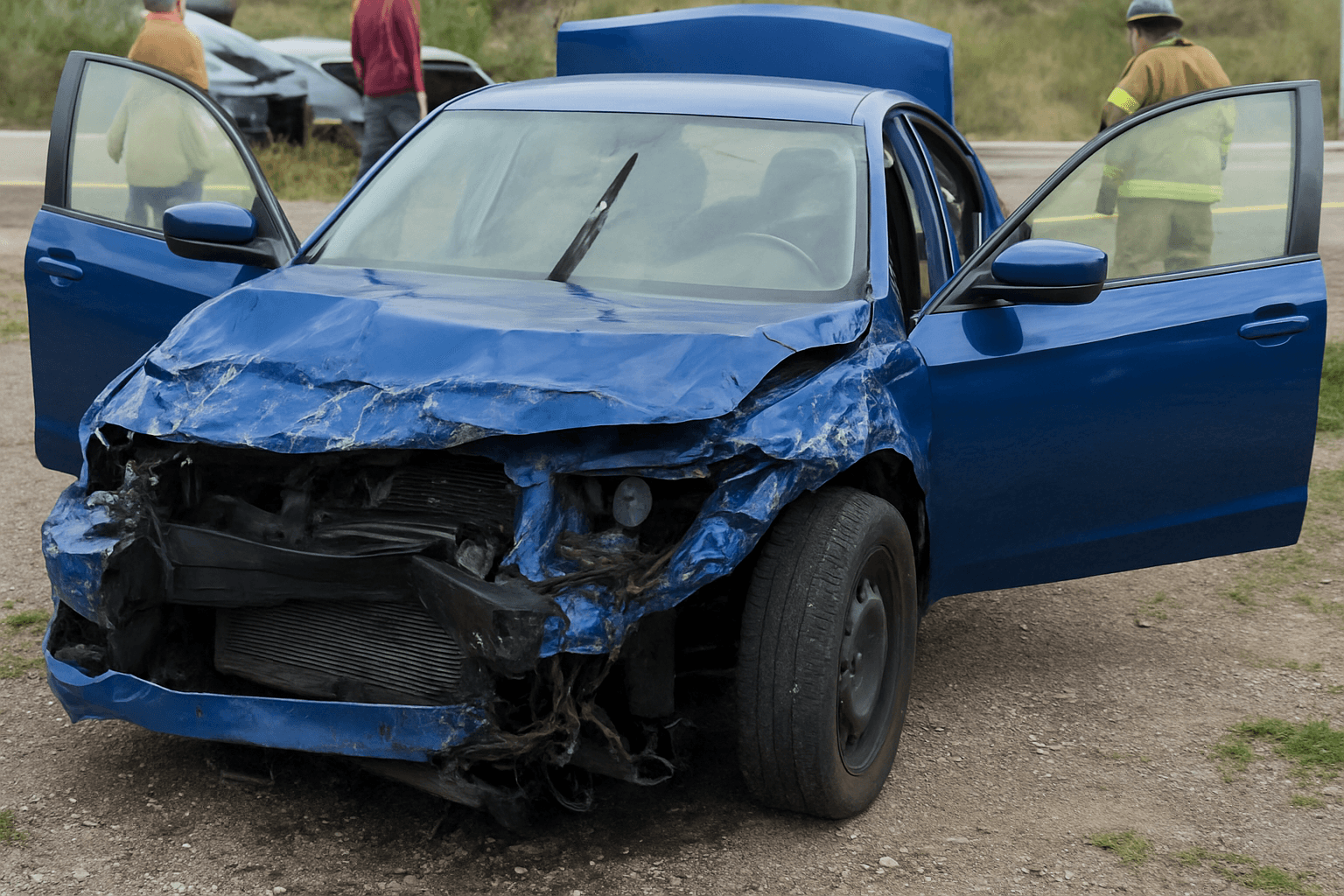

Liability insurance is the foundation of every auto insurance policy in Indiana. It covers the other driver's property damage and medical bills when you cause an accident. The numbers you see — 25/50/25 — represent thousands of dollars: $25,000 per person for bodily injury, $50,000 per accident total for bodily injury, and $25,000 for property damage. If you carry only liability coverage, you pay out of pocket for your own vehicle repairs and medical expenses after an at-fault accident.

- The other driver has $18,000 in medical bills and $6,500 in vehicle damage. Your liability coverage pays the $6,500 property damage in full and the $18,000 in medical bills, both within your policy limits. Your own bumper repair costs $3,200 — you pay that yourself unless you carry collision coverage. This is the most common suspended-license scenario: drivers who let coverage lapse and then cause an accident discover they owe reinstatement fees, SR-22 filing requirements, and potentially the full cost of both vehicles.

- The parked car has $4,800 in damage. If police identify you and you have liability coverage, your insurer pays the $4,800. If you do not have coverage, you pay out of pocket and face license suspension for driving uninsured. Indiana BMV suspends licenses immediately upon notification of an uninsured at-fault accident, and reinstatement requires proof of coverage plus SR-22 filing for three years from the reinstatement date.

- Your liability coverage does nothing in this scenario — the at-fault driver's liability insurance pays for your vehicle and medical bills. If that driver is uninsured or underinsured, you need uninsured motorist coverage to protect yourself. Liability-only policies leave you vulnerable in hit-and-run accidents and collisions with uninsured drivers, both common in Indiana.

Who Needs Liability Insurance Insurance?

You need liability insurance if you are seeking license reinstatement in Indiana after any suspension, even if you do not currently own a vehicle. Indiana BMV requires proof of continuous liability coverage and SR-22 filing for three years following DUI, reckless driving, excessive points, and uninsured accident suspensions. If you own a vehicle and plan to drive during reinstatement or after, liability is legally mandatory the moment you start the engine.

Start by confirming whether your suspension type requires SR-22 filing for reinstatement — call Indiana BMV or check your suspension notice. If SR-22 is required, you need liability coverage immediately to start the three-year clock. If you own a vehicle, get a standard liability policy. If you do not own a vehicle, get a non-owner liability policy. If SR-22 is not required but you need proof of insurance to reinstate, the same logic applies. Do not assume you can wait until after reinstatement to buy coverage — Indiana requires proof of continuous coverage during the entire reinstatement process for most violation-based suspensions.

How Much Does Liability Insurance Insurance Cost?

Liability-only policies in Indiana typically cost $45–$85 per month ($540–$1,020 annually) for drivers with suspended licenses seeking reinstatement. Non-owner liability policies, required for SR-22 filing without a vehicle, typically cost $30–$60 per month.

- Suspension reason — DUI suspensions increase liability premiums 60–120% compared to administrative suspensions for unpaid tickets or child support.

- SR-22 filing requirement — adding SR-22 to a liability policy adds $15–$35 per month in filing and risk fees.

- Coverage limits above state minimums — increasing from 25/50/25 to 50/100/50 typically adds $8–$15 per month but provides critical protection if you cause a serious accident.

- ZIP code — Indianapolis liability rates run 15–25% higher than rural Indiana counties due to accident frequency and uninsured driver rates.

- Driving record beyond suspension — each at-fault accident in the past three years adds 20–40% to liability premiums.

- Non-owner vs standard policy — non-owner liability costs 30–50% less than standard liability because it excludes vehicle coverage and limits exposure.